Why is ARM so expensive?

What’s the deal?

Why has ARM been acquired for over 20x historic revenue? The deal has made the headlines for a number of reasons: it’s a big one, valuing the chip designer at $40 billion; it’s controversial – customers worry that buyer Nvidia will have privileged access to new developments; and it’s further evidence of Softbank selling its crown jewels.

But little attention has been paid to the price.

What Factors influence THE arm deal multiple?

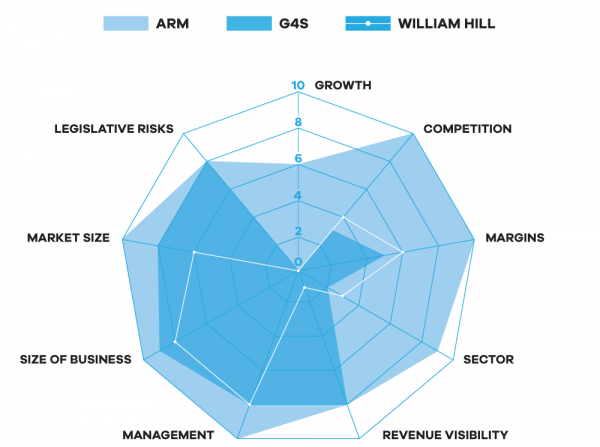

We plot ARM’s valuation drivers on the MarktoMarket Radar Chart. This shows (on a scale of 1 to 10) where ARM scores well and poorly. The bigger the volume of the company’s chart, the higher our expected multiple. For comparison, we have also charted two other recent takeover candidates, William Hill (betting shops) and G4S (security services).

The surface area for ARM tells us it is posting a high score on almost every metric. Every deal has its own nuances – if some commentators are correct, Nvidia is paying a big strategic premium to access ARM’s R&D earlier than their other customers, but the strategic value of an asset will vary from buyer to buyer. The criteria in our radar should be homogeneous across businesses and goes a long way to supporting ARM’s premium valuation.

arm valution radar chart

Sector

Industry characteristics influence price. Technology businesses like ARM will typically attract higher multiples than car dealers, for example. The former has IP, which should translate into higher barriers to entry and tends to deliver higher margins on greater degrees of revenue visibility (see below). Capital intensity will be lower, albeit will exist in the form of R&D, rather than investment in tangible assets.

Size

Bigger businesses attract higher multiples. ‘Bigger’ tends to equate to a longer track record, a greater degree of diversification of products and services, and a reduced propensity towards going bust (although shareholders in RBS may disagree with this). At $40 billion, ARM ticks the ‘big’ box.

Growth

Faster growth equals better prices. In a high growth business, profits will ‘grow into’ a multiple. Conversely, a low growth company will look expensive for a long time if a punchy entry multiple is paid. ARM’s compound annual growth has been impressive, but revenue progress has tapered in recent years: Nvidia will be expecting to reverse this.

Market Size

Is the target company going after a massive end market opportunity? Or do revenues ‘cap out’ at a more modest level because the addressable market is too niche? The prospect of chasing a lucrative, usually global, prize will convince buyers to stretch their valuation. The global smartphone industry? That’s a monster of a market.

Competition

Related to market size is the question of whether that market is crowded or whether the target business has a monopoly. If there is no competition, there may be a good reason (the market is too small – see above). Alternatively, potential rivals may have missed the opportunity or decided that the barriers to entry are too great. If it’s the latter, buyers should be paying a hefty premium. ARM has competition, including RISC-V, an open-source semiconductor architecture, but still dominates the market for low-power, efficient smartphone chips. It describes itself as “the R&D department for the semiconductor industry” – which sums it up quite neatly.

Revenue Visibility

Related to sector, greater revenue visibility translates into lower risk which equals higher price. Discounting at a lower rate will return a higher valuation. Simple. ARM receives upfront licence fees, followed by royalties on every chip sold with its technology embedded. Its royalty revenue can be forecast by reference to its predicted smartphone sales.

Margins

Related to sector and competition, higher margins suggest a strong offering that customers are willing to pay up for. A huge market plus limited competition should allow you to pick your pricing and drive enviable margins.

Management

Has the management team delivered before? In ARM’s case the answer is yes. CEO Simon Segars was one of ARM’s first employees and oversaw its transition from publicly listed stock to Softbank portfolio company.

Legislation

If one thing can kill a business in a heartbeat it is legislation. Industries subject to scrutiny, such as gambling, run the perennial risk of outside intervention. With this risk comes uncertainty around how to plan and forecast. The industry in which ARM operates is less controversial but, as a great British technology success story in the process of a deal with possible competition and job consequences, it has attracted the attention of the regulators.

Like this post? Check out our other Deal Insights.